The Commodification of Validation

Validation as a service has become more commodified just as the infrastructure and capacity to run validator companies has become more bespoke and esoteric, with higher barriers to entry

Validation, and node operation as we know it feels like it is approaching an endgame.

Obviously, I have pretty strong opinions and experience in this area; our first Needlecast blockchain node came online almost exactly five years ago. I don’t know what the exact definition of crypto survivor is, but I’ve got a reasonable claim to having weathered some pretty big busts, hacks and insane situations.1

In the naïve view, validators should be fungible.

In an old episode of the validator podcast we periodically did with Lavender 5, Rhinostake and Kingnodes2 we hypothesised, probably around 2022, that the validator business would gradually become a margins game. I’m pretty sure we even presented a Wardley map to show how the validator business was maturing in the direction of being a commodity—if you like Wardley maps, then stick around.3

Since then, the dominant narrative has been one of consolidation; of mergers and acquisitions among the larger independent players, bankruptcy for those that overreached in various bull runs, and a long tail of smaller independent or hobbyist validators.

We’ve sat uneasily in this narrative, because of course we are not one of the larger independents (although some of our close colleagues such as L5 or Polkachu might sit in that category), but have also at some times had something under the order of half a billion USD in Assets Under Stake (AUS). Still, it has felt for a while like our time is limited, as a more boutique operation in a higher-cost jurisdiction.

This in itself isn’t that big a deal. In the naïve view, validators should be fungible, and perhaps it should be a margins game (whether we’re talking about PoS or DPoS4—Ethereum has been a margins game for some time, even with MEV factored in).5 However, the reality is that if you care about a metric like geographic decentralization, or indeed datacentre or infrastructure decentralization (and blockchain Foundations seem to), then validators are not fungible. Not only that, but their running costs are widely variable depending on location and juristiction.

For example, as mentioned before, if you’re in a high-cost jurisdiction, not only are your baseline costs (salaries, utilities, fees, legal, accountancy, business support, et cetera) higher, but there’s also typically more of a regulatory presence. In the UK this has always loomed, albeit somewhat inconclusively. Luckily for us HMRC published a comprehensive tax manual for businesses quite early on, so compliance on that front hasn’t been too big an issue,6 but elsewhere we have still had problems.

Chief among these is debanking. Although we’ve not run a regulated operation7 and any stakers custody their own funds,8 working in this space paints a risk target on your back that results in periodic interruptions to business operations. We’ve had to at various times run multiple different bank accounts, and eventually we fully split the business operationally to address this risk.

The end result is more cost, not only in accounting and admin, but also if you need, for example, banking providers that will deal with high-risk clients. Such arrangements (these typically require a base deposit level of $25k or more) are expensive and also effectively lock up operational cash. These considerations are all part of the service that implicitly our clients and counterparties receive, though they don’t pay for it, per se.

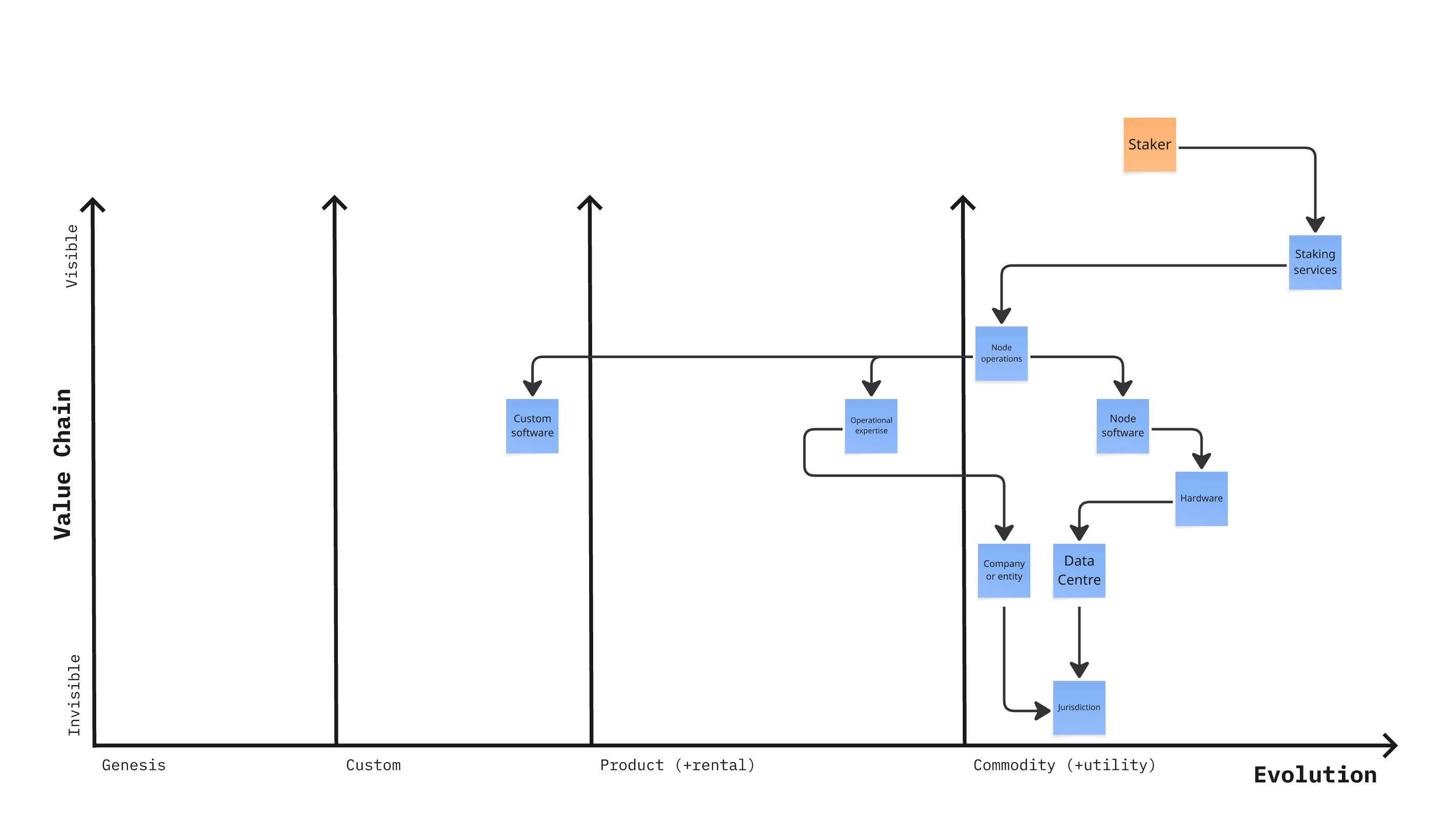

In fact, typically none of this is factored in by counterparties. In the two Wardley maps below,9 I’ve taken a rough approach at sketching out the value chain for validation. For consumer-level stakers, they often don’t care where a validator is based, or what their setup is. They just care about uptime and cost. This means they see the operational expertise as slightly less commodified, yet there’s not much custom beyond a brand.10 Most validators have some degree of custom software, even if it’s just for monitoring, that’s not something stakers will typically pay for.11

As an independent node operator in this space, you’re competing with major CEXs, some of which are regulated, with a huge brand presence. Given that performative aspects of blockchains tend to get the most attention (not that this is different in other industries, to be fair) marketing and brand has an outsize impact, and it’s no surprise as a result that few independents can compete in the consumer staker market over the long run.

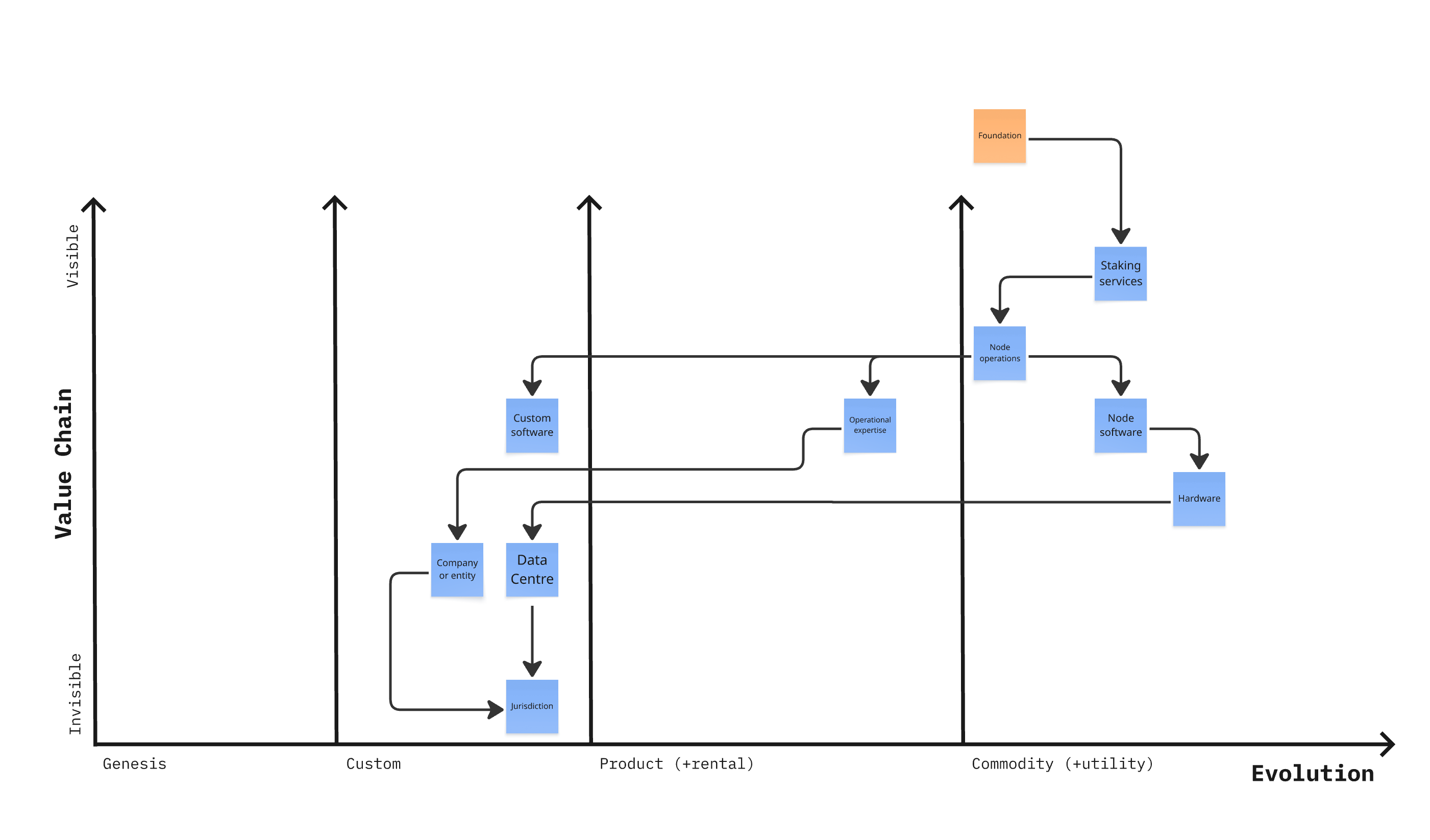

You could draw this map differently based on what stakers perceive, or want, from the value chain, versus what it actually looks like. From the perspective of the operator, it looks like the Foundation Wardley map, below, in both cases, but only in the Foundation case are the custom elements typically compensated at all.12

Foundations, unlike stakers, typically care intensely about certain aspects of operations, going out of their way (in most cases) to KYC and vet their counterparties and the companies they delegate to, while (often) also specifying desired jurisdictions and node locations.

This is a highly custom service, and yet often it does not come with the recognition of it as such. It’s not exactly clear why; maybe validators are all bad at negotiating, or maybe it will take a sustained bear market cull to re-establish the perception of what is, effectively a subtype of institutional validation as an appropriately expensive service, rather than the commodity service it is in the case of DPoS.

As you can see, it’s hard to represent by abstractly placing ‘validation as a service’ on a Wardley map,13 and I suspect, regulators have little sympathy.14 Regulators probably assume all validators are raking in cash and are mainly focussed on the big operators.

As we’ve seen just in the last weeks, future regulation in Korea has likely been part of the reason that a large validator, a41, has decided to exit—and they didn’t exactly seem to be struggling. As validators, and particuarly as independent validators, we need to become better at articulating what exactly it is that clients, stakers, or counterparties are actually paying for. In some cases, we still need to make the case that they need to pay for these things at all.

Still, this all may represent an opportunity. With validators exiting both via merger and bankruptcy, market stresses or regulation, it might be that there’s more opportunities for small, leaner or mid-tier validators to pick up market share. Whether or not that will pan out into a more predictable or scalable business model in the long-run remains to be seen.

Off the top of my head, Juno Prop 16 (complete timeline of the craziness here), the Terra/LUNA crash and slow implosion of the Cosmos Ecosystem, to name a couple. Weathering bear markets is less headline-worthy, but it’s a swingy business and we know a lot of validators that have either gone bust or exited.

Very occasional these days due to timezones and family commitments, but there are about 150 episodes as a result of our previous weekly schedule.

There’s also some crossover with the business commandment over not choosing business ideas with a low barrier to entry, from The Millionare Fastlane by MJ DeMarco. Indeed, for this (and other reasons—I suspect, for instance, the number of companies in the space that appear to overreach and then fail means validation may not be as scalable a business as you might intuit) I have a tiny bit of sympathy for the arsehole who once told me I don’t “run a real company” at a fintech meetup.

Proof-of-Stake (PoS) or Delegated Proof-of-Stake (DPoS); think, single-value staking, or pool staking/bonded stake. Ethereum is PoS, Cosmos and many other newer networks like Monad are DPoS.

If you want a detailed description of these, try Bashir (2022). For now, sufficient to say that Ethereum is PoS, Aptos is PoS—although staking pools exist, and Cosmos and Monad are DPoS, to use a few examples.

Although it has been complex in terms of finding good accountants et cetera. Moreover, some users seem to not understand that any companies in the space actually pay their taxes. Try telling an angry degen in a Telegram chat that your dev team doesn’t have nearly as much funding as they assume because you paid the correct amount of tax—you won’t get much sympathy. Additionally, the reason this is different from just selling widgets, or pencils is that you’re also expected to re-stake some portion of protocol revenue, even if the penalty is mainly social. Perhaps to our error we bowed to pressure to re-stake a portion of proceeds. When you re-stake, you pay tax at that value, so we paid full tax on the value of tokens that are now worth basically zero. The loss is listed against cap gains, so isn’t even useful operationally. Lesson learned.

In any case, a lot of our work for the first couple of years was protocol development rather than validation—Foundation delegations to a validator were often simply incentive alignment rather than intended to be in lieu of payment, either by dev grants or directly via protocol revenue.

And indeed the majority of our AUS and business has been predicated on Foundations and Core Teams staking with us.

Those that have worked with me as a consultant will recognise Wardley mapping—yes, I do apply it to my own business ventures.

I haven’t put ‘brand’ on these Wardley maps, but I guess it would be toward the top (highly visible) and in the custom quadrant, as mentioned.

As anybody that lived through Cosmos’ appchain winter will know, the most valuable custom software is a rinse-and-repeat staking interface that users can use on network genesis, with your validator auto-selected as the choice. These were ubiquitous at that time.

On this topic, in our paper on Decentralization, an interviewed node operator summarised, “nobody’s going to pay for it, I’ll tell you that.”

This is the argument for placing ‘validation’ in the ‘commodity’ quadrant, but the actual business and support/associated services that are potentially more hidden in the value chain in the ‘bespoke’ quadrant. Perhaps even further to the left. See? Wardley maps do work!

I sympathise with them.